How to Choose a Travel Card for Backpackers

When traveling, it’s crucial to pay close attention to the costs associated with managing your money. Many people use cards or accounts that, aside from fixed fees, impose substantial charges. For international cash withdrawals, many traditional accounts and cards often levy fees of 5€ or more on each withdrawal. Additionally, foreign currency payments can incur a 3% markup on the exchange rate. Clearly, these fees can significantly impact your budget, especially for long-term travel.

This article outlines which solutions to choose and why it’s essential to minimize these costs. I strongly recommend reading the entire article to understand why I recommend specific accounts and how to avoid various fees, which can extend beyond simply having the right card.

Remember to cover the keypad with your hands when withdrawing!

Understanding Different Card Types: Debit, Credit, and Prepaid

First, let’s clarify some terminology starting with the word “ATM,” which I often use in this article: ATMs are simply cash machines. When I refer to interbank exchange rates, I mean the “official exchange rate” or “commission-free currency exchange rate,” which is the rate shown by various apps or Google searches. Ideally, this is the rate you would like to have for withdrawals, online payments, or transactions at a store or restaurant.

Debit Card

A debit card is linked to a checking account. When you make a purchase online, pay with the card, or withdraw cash at an ATM, the amount is directly deducted from your account balance. If there are insufficient funds, the transaction will fail. Despite the widespread belief that a credit card is necessary for travel, a debit card is often sufficient and the best choice for most people. The only situation where you might require a credit card is if you plan to rent a car. I have traveled exclusively using debit cards for years and have never encountered any problems.

Prepaid Card

Prepaid cards function similarly to debit cards. When making online purchases, paying with the card, or withdrawing cash from an ATM, the funds are directly deducted from the card account. Therefore, the transaction’s success depends solely on the available balance at that time.

While prepaid cards were once popular, especially for online transactions when traditional debit cards lacked this feature, they are now considered outdated. Prepaid cards often come with fees for reloading, management, and issuance. Additionally, their functionality and banking options are limited compared to a checking account. In summary, debit cards are a superior choice compared to prepaid cards. They do not have the drawbacks associated with prepaid cards and offer greater functionality.

If you are concerned about the security of your funds in the event of card cloning or theft, you can achieve the same level of security with a debit card. Simply use the checking account linked to the debit card as if it were a prepaid card. “Top up” the account through wire transfers only when needed. This is the approach I take with all my travel accounts where I keep minimal funds. Meanwhile, my primary savings remain secure, protected from potential fraud or theft.

Credit Card

Credit cards function differently from debit and prepaid cards in that they are not directly linked to a checking account. Instead, transactions are recorded and you settle the balance later. With a credit card, you can make withdrawals or payments without having sufficient funds in your bank account. The bank or card issuer covers the amount and you are billed for it at the end of the billing cycle, usually the following month. However, if you don’t have enough funds to cover the statement balance, you’ll face high-interest rates and risk having your card revoked eventually.

Getting a credit card isn’t guaranteed. You typically need to demonstrate a certifiable income and have a good credit history. It’s also challenging to find a credit card without fees or spending constraints, except for a few exceptions. Credit cards generally don’t offer favorable terms for cash withdrawals. For most people, having a credit card might be an unnecessary expense unless they make large purchases and benefit from good rewards programs, which are common in the US.

In summary, for backpacking, a reliable debit card paired with a good checking account is often the best choice. That’s why most of the options recommended in this article fall within this category.

Choosing an Appropriate Card for Backpacking

As I see it, there are only three aspects to consider:

Fixed and Account Management Fees: These include all the costs of maintaining the account or card, such as monthly/annual fees, recharge transactions, transfers, account opening, etc.

Withdrawal Fees: While it is generally free if you withdraw at your bank’s ATM, it can be expensive at other banks, especially if you are withdrawing in a different currency. For example, most bank accounts in Italy offer free withdrawals throughout Europe. However, as soon as you leave European borders, you might be charged up to €5 per withdrawal plus a currency exchange fee.

Currency Exchange Fees: These fees are charged in addition to withdrawal fees when cash is withdrawn in a different currency, normally varying between 1.5% – 3% of the amount or based on the exchange rate, and are often “hidden.” They also apply to payments in foreign currency.

Other Helpful Tips for Avoiding Bank Fees

It’s essential to be aware of potential fees charged by local banks when using foreign cards abroad. These fees may not depend on your specific account or card and can be challenging to avoid in some countries. One strategy to mitigate these fees is to withdraw larger amounts in a single transaction whenever possible.

You can also search online for information on banks in a specific country that offer free withdrawals for foreign cards. Try Googling ‘name-country ATM no fee”. Many websites or forums provide this information, helping you find the most cost-effective options.

When using ATMs abroad, always decline any offers to convert the transaction amount into your home currency. Opt to complete the transaction in the local currency to ensure you get a more favorable exchange rate from your bank or card provider.

Additionally, when making online payments in foreign currencies, be cautious of platforms that apply their exchange rates, which may not be favorable. Always choose to pay in the currency in which the price is expressed and allow your bank to handle the currency conversion, provided they don’t charge additional fees for such transactions.

For example, if you’re purchasing an item from a website based in England, ensure you pay in pounds sterling rather than allowing the platform to convert the amount to euros at a disadvantageous rate.

Best Travel Cards for Backpackers: Top Picks for 2025

- Revolut

- Wise

- N26

- Curve

- Trade Republic (referral code: grj0l4ps)

In case it hasn’t become clear yet, I am a savings freak and have spent days reading fact sheets of numerous accounts to figure out which are currently the best solutions for traveling and, most importantly, withdrawing cash abroad without spending a fortune. This is especially important because, in developing countries, card payments are rarely accepted. That being said, not all the listed options are available worldwide. If you happen to live in a country where you can’t get your hands on any of these accounts, I recommend doing some research using what you have learned so far in this guide.

N.B. Although there is one account that, in my view, is superior to all others, especially for those who travel long term, never rely on a single card, especially abroad!

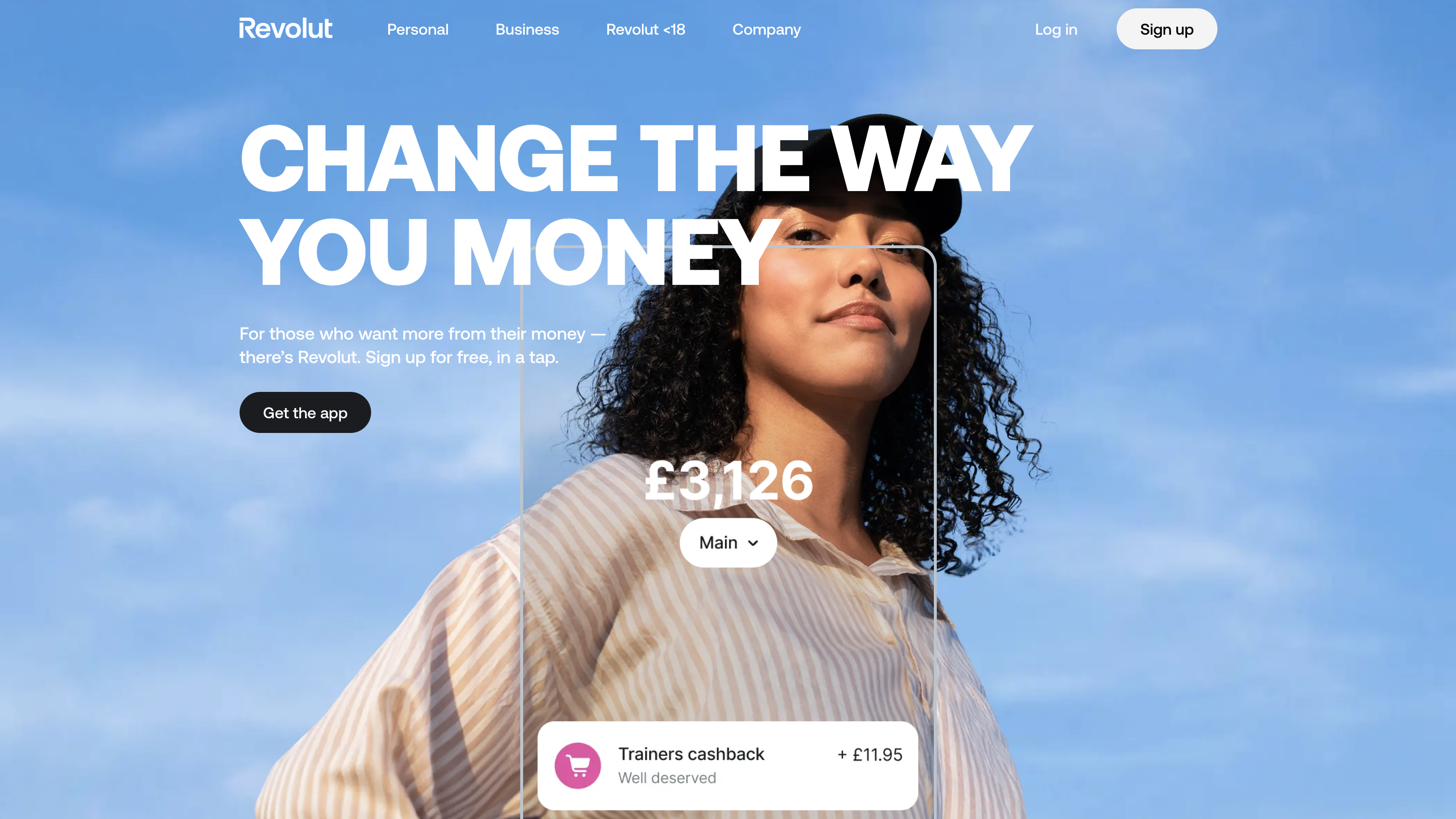

Revolut Account Review

Four versions are offered: one free called Standard, and three paid versions called Plus (€2.99 per month), Premium (€7.99 per month), and Metal (€13.99 per month).

The free version has no monthly fee (£4.99 for issuing the card), offers payments without any surcharge on the exchange rate for over 150 currencies, and international transfers at the interbank exchange rate in over 29 currencies up to a total of €1,000 per month (after which a 1% fee is charged). There is an additional 1% weekend fee for currency exchange. It also includes completely free worldwide withdrawals up to €200 per month, after which a 2% fee is charged on the amount withdrawn, with a minimum of €1. Note that the commission is also applied if you exceed five monthly withdrawals while remaining under the €200 total.

The Plus version is, in my opinion, the least interesting of all. With a fee of €3.99 per month, you basically get insurance for online purchases up to €1,000 per year and a 0.5% weekend fee for currency exchange. Otherwise, the conditions are pretty much the same as the free version.

The Premium version (€8.99 per month), compared to the free version, offers unlimited international transfers and unlimited payments at the interbank exchange rate in over 29 countries and 150 currencies, respectively. There is no additional weekend fees for currency exchange. The free version’s limit of €1,000 per month for payments and transfers is removed. It includes completely free worldwide withdrawals up to €400 per month, after which a 2% fee is charged on the amount withdrawn (with a minimum of €1). Disposable virtual cards are also included, and travel insurance is part of the monthly payment. This insurance covers emergency medical and dental care worldwide, as well as reimbursement for travel and luggage delays, directly to your Revolut account.

Although the insurance is included in the fee, I honestly don’t think it is worth €7.99 per month; I would recommend separate travel insurance. Also, keep in mind that the maximum trip duration covered is 90 days per trip. If you travel for longer, you’ll be covered for the first 90 days only. The appealing aspect is the free withdrawals up to €400, but again, I don’t think the extra €200 is worth the monthly fee.

Some people might find the Metal version interesting (€15.99 per month). In addition to everything offered by the Premium version, it raises the limit of free withdrawals up to €800 per month (after which a 2% fee is charged on the amount withdrawn with a minimum of €1). Most importantly, it offers up to 0.1% cashback in Europe and up to 1% outside Europe for every payment made by card. So, if you travel a lot and pay large amounts with the card, the cashback alone could cover the monthly fee!

The Ultra version (€45 per month), I believe, has a monthly cost that few can justify. I think it is designed more for those who use the account to manage their investments as well. In any case, the limit of free withdrawals is raised to €2,000 per month. I recommend the Standard account, but if you travel often and pay large sums of money with the card, the Metal version is interesting; the Premium version seems like a “rip-off” to me. Also appealing is the possibility of choosing between Visa and Mastercard when ordering the card (it used to be offered in the past. Now, the selection is automatic based on the geographic area). Finally, unlimited virtual disposable cards are offered with all plans, a handy feature if you have to make online payments on sites you deem untrustworthy.

N.B. When you read that Revolut does not support a currency, it only means that the possibility of having a balance in that particular currency is not offered. You can still make transactions such as withdrawals or payments!

Summing up:

- No monthly fee for the Revolut Standard account (£4.99 for card issue), €3.99 Plus, €8.99 Premium, €15.99 Metal, and €45 Ultra.

- International transfers and payments at the interbank exchange rate in over 29 and 150 currencies, respectively, up to €1,000 per month, after which you pay a 1% fee for the Standard and Plus accounts; for Premium and Metal, there is no monthly limit.

- Completely free worldwide withdrawals up to €200 per month for Standard and Plus accounts, €400 for Premium accounts, €800 for Metal accounts, and €2,000 for Ultra accounts, after which you pay a 2% fee on the amount withdrawn.

- There is no exchange rate surcharge for transactions in more than 150 currencies, excluding weekends.

- Travel insurance is included in Premium, Metal, and Ultra accounts.

- The Metal account offers 0.1% cashback in Europe and up to 1% outside Europe for every payment made, plus a free pass that can be used in more than 1,000 airport lounge areas worldwide.

Wise Account Review

Wise (formerly TransferWise) is an excellent service for transferring money between bank accounts in different currencies. Their fees are among the most competitive in the market.

Wise also provides a unique, completely free account. This account allows you to hold and manage over 40 currencies simultaneously, with low fees for converting them within the account or making transfers to other accounts.

The platform offers a transparent cost calculator that allows you to simulate any transfer or currency conversion and see the fees upfront. For frequent transfers in currencies other than the euro, Atlantic Money might be worth considering. While they support fewer currencies than Wise, they offer a flat fee of €3, making them potentially cheaper for large transfers.

However, the main focus of this review is the debit card associated with the Wise account, which offers several attractive features. The card utilizes the Mastercard network and is free (with a one-time €7 issuance fee), just like the account itself. When using the card for payments in a currency you hold in your account, there are no additional exchange rate fees. Essentially, free payments in any account currency.

There are fees, however, for spending in currencies you don’t hold in your account, ranging from 0.35% to 2%. In such cases, using a card from N26 or Revolut (on weekdays) might be a better option.

What truly sets the Wise card apart is the ability to withdraw any currency for free twice a month, as long as the total amount withdrawn stays under €200 (or the equivalent in your account currency). However, exceeding the free limit incurs a small fee: €0.50 per withdrawal plus 1.75% of the withdrawn amount. Similar to Revolut, Wise also allows you to create virtual disposable cards (up to three at a time).

Important Note: When Wise says they don’t support a particular currency, it only means you can’t hold a balance in that currency. You can still make transactions like withdrawals or payments in that currency!

Summary:

- No monthly fees, €7 one-time fee for card issuance.

- Hold and manage over 40 currencies in the account. Make and receive international transfers at competitive rates.

- Free debit card with Mastercard network. Two free ATM withdrawals worldwide up to €200 every 30 days. After that, €0.50 + 1.75% fee applies.

- Free currency exchange for payments in account currencies. 0.35% to 2% fee applies for other currencies.

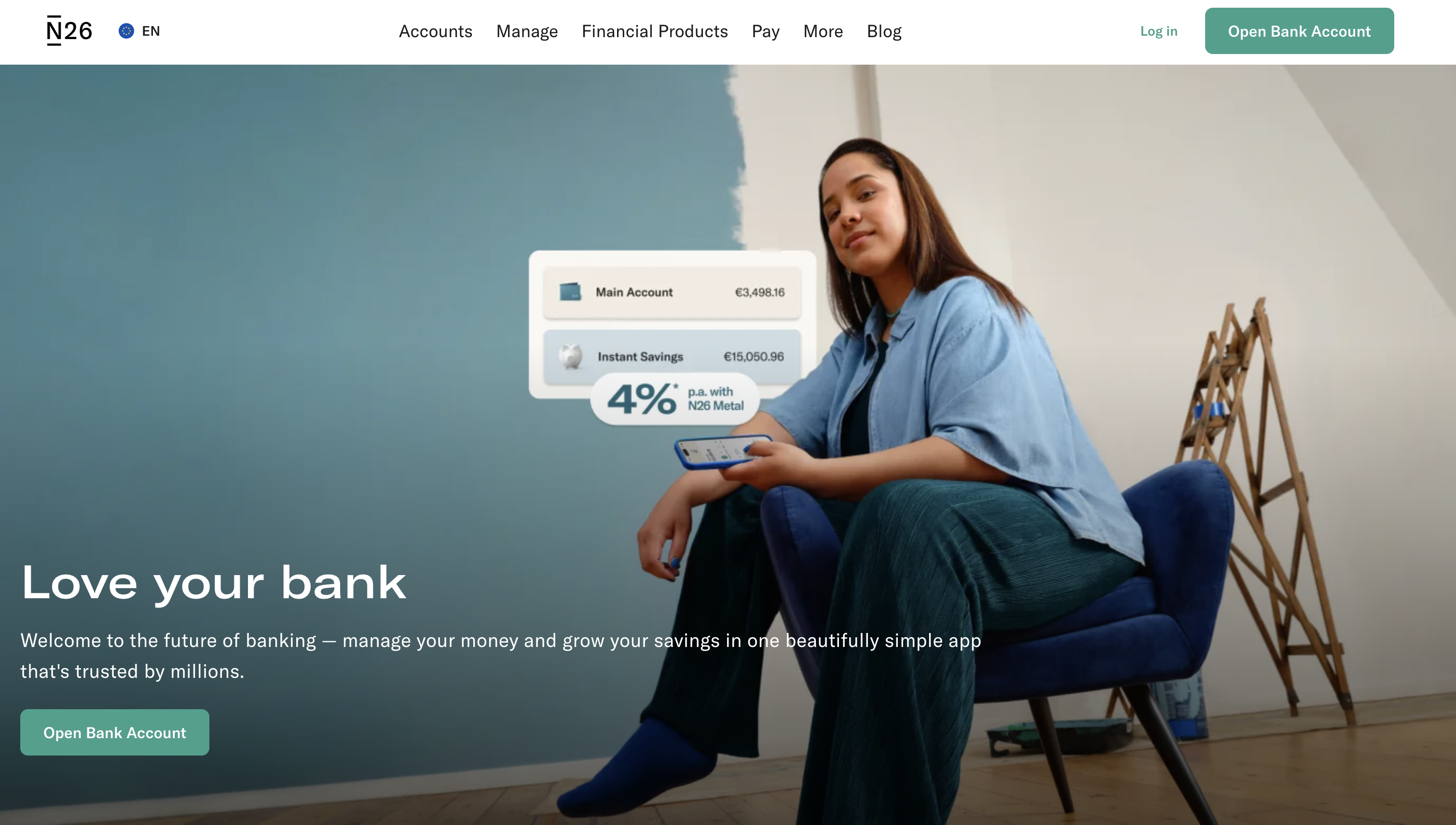

Review Account N26

N26 is another fascinating fully online account; three versions are offered: one free, called N26 Standard, and three paid versions, called N26 Smart (€4.90 per month), N26 You (€9.90 per month), and N26 Metal (€16.90 per month).

The standard N26 version has no monthly fee (€10 for card issuance). It offers free withdrawals worldwide but charges a currency exchange fee of 1.7% on the amount withdrawn. Essentially, it offers completely free withdrawals (3 per month) throughout Europe and a 1.7% fee on amounts withdrawn outside the eurozone. The highlight of this account is that it does not charge any surcharge on the exchange rate for transactions in currencies other than the euro, and the card uses the Mastercard circuit.

N26 Smart, somewhat like Revolut Plus, is the least attractive account; the €4.90 per month fee only adds the possibility of having a second debit card, sharing savings accounts with other users, access to “exclusive discounts,” and support via phone. In my opinion, it is not worth it.

The N26 You account costs €9.90 per month, but in this case, it offers free withdrawals worldwide with no currency exchange fees. The monthly payment of €9.90, in addition to withdrawals without currency exchange fees, includes travel insurance in cooperation with Allianz.

It is a reasonably comprehensive travel insurance that covers medical expenses, airplane or baggage delays, cash theft (you receive a refund if the theft occurs within 4 hours of withdrawal with your N26 You card), liability limitations, and more.

You can find the fact sheet on this page. Nevertheless, this is not a bad travel insurance policy; it should be more than enough for most people. Considering the cost of insurance taken out separately, it should be clear why I think the N26 account is an excellent solution.

If you decide to opt for this account, keep in mind that you are insured for a maximum period of 90 days from the time you leave your home country.

In any case, it is an excellent solution that I recommend, especially in the paid version, to those who make one or more trips during the year without exceeding 90 days. The money saved on travel insurance and withdrawal costs more than repays the monthly fee.

Summing up:

- No monthly account fees for N26 Standard (10€ for card issuance), 4.90€ for N26 Smart, 9.90€ for N26 You, and 16.90€ for Metal.

- Free Euro Withdrawals.

- Fees for withdrawals in currencies other than the Euro: N26 Standard and Smart charge 1.7% of the amount withdrawn, while N26 You and Metal Accounts are free of charge.

- No currency exchange fees for payments.

- Travel insurance is included with N26 You and N26 Metal paid accounts.

Curve Review

Curve offers a truly revolutionary and exciting service. It is not a bank account but rather a card that can be linked to as many cards as you want (currently Mastercard or Visa), forming a virtual wallet of all your cards.

Once you’ve entered your card details via the smartphone app into this virtual wallet, you can choose which one to use. When you make a payment or withdrawal with your Curve card, the money will be deducted from the selected card, which you can change at any time.

This is incredibly convenient for two reasons: firstly, you can make transactions and track expenses across your various accounts using just one card; secondly, when you make transactions in currencies other than the euro or pounds, Curve applies the interbank exchange rate to the transaction before charging the linked card. This is advantageous if you have cards that typically charge currency exchange fees. The same applies to withdrawals.

Another exciting feature is “Curve Customer Protection,” which covers you for unauthorized purchases up to €100,000. If you encounter problems with a product or service purchased with the Curve Card, it initiates a dispute with the retailer, similar to many credit cards.

Curve offers four versions: a free one called Curve Standard and three paid versions called Curve X (€4.99 per month), Curve Black (€9.99 per month), and Curve Metal (€14.99 per month).

In summary:

Curve Standard is entirely free (card issuance costs €5.99) and allows you to spend up to €250 per month on currency exchange, after which a 2% fee is charged. Withdrawals cost €2 or 2% of the amount withdrawn, whichever is higher. This was a plan I had recommended in the past since the economic conditions were much better, but at present, I believe there are significantly better options.

Curve X costs €5.99 per month and allows you to link up to 5 cards. It allows you to spend up to €1,000 per month in currency exchange without fees and €300 in withdrawals. Once these amounts are exceeded, the same conditions apply as for the Curve Standard. Even this option, I think, is really unattractive.

Curve Black costs €9.99 per month, raising the threshold to €2,000 per month for currency exchange payments and €500 for free withdrawals. Once these figures are exceeded, the same conditions apply as for the Curve Standard. Cashback of 1% is offered on six retailers.

Curve Metal costs €17.99 per month, removes the limit for currency exchange payments, and raises the threshold to €1,000 per month for free withdrawals. Once these figures are exceeded, the same conditions apply for the Curve Standard. Cashback is offered on twelve retailers of your choice compared to Curve Black’s six. With Curve Metal, you also have access to airport lounges.

Summing up

- No monthly fee for Curve Standard account, €5.99 for Curve X, €9.99 for Curve Black, and €17.99 for Curve Metal.

- There is no exchange fees for transactions in currencies other than the euro up to €250 per month with Curve Standard, €1,000 with Curve X, €2,000 with Curve Black, and unlimited with Curve Metal.

- Completely free worldwide withdrawals up to €300 with Curve X, €500 with Curve Black, and €1,000 with Curve Metal, after which you pay a 2% fee on the amount withdrawn or £2 (whichever is higher).

- Cashback of 1% on six retailers forever with Curve Black and twelve retailers forever with Curve Metal.

- Access to airport lounges with Curve Metal.

Trade Republic Account Review

You can get €10 in shares after making two investments by entering the code: grj0l4ps

Trade Republic started as an investment broker, but today, it can be considered a fully-fledged bank account with unique economic conditions. Let’s delve into why the debit card associated with the Trade Republic account is, in fact, the best solution for most travelers. The account entails no monthly fees (though the card costs €5 to issue), no fee for currency exchange transactions, and offers free withdrawals for amounts over €100 (or the foreign currency equivalent). For withdrawals of amounts under €100, there is a minimal fee of only €1.

Additionally, there’s an opportunity to earn 1 percent in what Trade Republic calls “Saveback,” a special cashback applied to payments made with the card, which goes into your savings plan. To qualify, you need to have set up a savings plan of at least €50 per month. Saveback applies to the first €1500 monthly, allowing you to earn a maximum of €15 monthly.

This is an exceptional product, not only ideal as a travel card but also for managing liquidity, given the 4 percent interest on deposited amounts and the possibility of investments through completely free savings plans.

Summing up:

- No monthly fees.

- 2,25% interest on sums deposited up to €50,000.

- No Currency Exchange Fees.

- Free withdrawals for amounts over €100 (or foreign currency equivalent).

- Completely free accumulation plans on ETFs or stocks.

- Invest with as little as €1 in stocks, ETFs, or cryptocurrencies.

Final considerations

I strongly advise against traveling with only one card. Ideally, it would be better to have a Visa and a Mastercard. If you want to avoid paying foreign bank fees and unpleasant situations (such as the card not being accepted, getting demagnetized, or stolen), I recommend the following:

- To completely eliminate fixed costs, use Trade Republic and at least one of Wise or Revolut. With these three cards, you have zero fixed costs and unlimited free withdrawals. If you only want one card, Trade Republic is the best option, but Revolut is also acceptable.

- If fixed costs are not an issue and you want to withdraw and make currency exchange transactions for free without fees and enjoy some extra benefits, N26 You and Revolut Metal are probably the best solutions. However, even then, I would pair at least one other card with it.

The “ultimate” solution does not exist; there are those who travel in specific contexts and manage to always pay with a card, those who rely solely on cash, those who prefer to pay a monthly fee and have a single account, and those who like to rely on multiple free accounts while minimizing costs, and those who want lounge access, cashback, and so on. Make your own considerations.

One last piece of advice: when you go on a trip, don’t rely solely on cards; always try to have some emergency cash with you; euros are generally easy to change, although U.S. dollars are usually a better choice. If you have any questions or know of any other travel accounts or cards worth mentioning, please feel free to leave a comment!

P.S. If you found this article helpful, consider opening your accounts via one of the affiliate links on this page. (If you don’t see them, turn off Ad Blocker.) Doing so supports the site at no additional cost to you. Thank you!For donations/pizzas and virtual beers 🙂

Did you like the post? Pin it!